Australia will have the luxury to be one of the first countries to transition to renewable energy sources in accordance with the Paris Agreement, but in parallel, we also have a responsibility to keep the supply and some comfort of living standards for lesser developed countries still dependent on Australian coal and gas. It has been argued that we need to transition to climate-friendly energy sources immediately; however, energy storage at scale and effective sources of alternative climate-friendly energy are still being developed and yet to be proven, so we need to responsibly manage risk and consider a program that can get us all to where we need to be. A clear and responsible plan for cutovers to sustainable effective energy sources is critical; fundamentally, all people need a reliable power supply. Let’s not make decisions today that risk people suffering tomorrow.

Driving the current surge in resources and energy export earnings is a spike in energy prices and the Australian dollar’s weakness against the US dollar. Energy prices are elevated largely because of a looming drop in exports of gas, coal and oil by Russia, one of the world’s largest energy exporters.

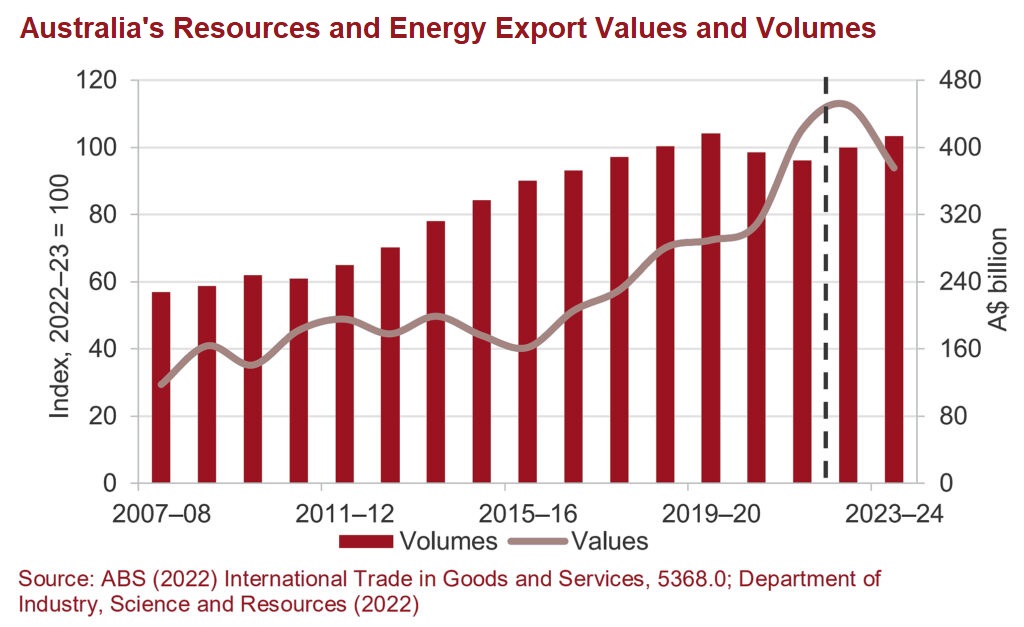

Australia’s resources and energy export earnings are forecast to reach $450bn in 2022–23, surpassing last year’s record of $422bn. Earnings are then forecast to fall to $375bn in 2023–24 (which is still ‘great’ as it shapes up as the third-highest on record) as world supply responds to high prices amidst a soft demand backdrop.

Energy prices are elevated largely because of the conflict in Ukraine, which has impacted gas, coal and oil prices given Russia is one of the world’s largest energy exporters. By early 2023, the market for Russian exports will have shrunk noticeably; transport and infrastructure constraints will likely prevent a full diversion of some of these energy commodities from the West to nations such as China and India. The net result is a drop in world energy supply as some Russian output becomes stranded. We then expect the prices of energy commodities to remain high and may accelerate the push towards the adoption of low emission technologies.

Australia is well placed in the global push towards low emission technologies. Exports of metals used intensively in low emission technologies, namely copper, nickel and lithium, are expected to generate $33bn in export earnings in 2022–23, over double what was earned in 2020–21.

Gas, LNG and thermal coal prices are already at record levels and as adverse weather patterns like La Niña flooding in Australia’s eastern states and drought impacting large parts of Western Europe, the US, Southern China as well as the upcoming Northern Hemisphere winter months will again ensure high commodity prices. LNG and coal earnings are forecast to be two to three times higher than in 2020–21, with earnings from these commodities being likely to fall back towards pre-pandemic levels after 2023–24 as supply improves.

Iron ore prices have fallen recently by around 20% in the September 2022 quarter. Combining growing global recessionary fears, new COVID-19 lockdowns and weakness in China’s housing sector, world steel and iron ore demand have dampened in recent months.

In the September 2022 quarter, the Office of the Chief Economist’s Resources and Energy Export Values Index rose 25% from the previous year; a small rise in volumes added to a 24% gain in prices.

In terms of risk, there are some to keep in mind.

As we look forward to record export earnings forecasts, we need to be mindful there are some current risks like global inflation, interest rates, resistant strains of coronavirus and further geopolitical disruptions with China and Russia. Despite these risks, my main concern is with the current ‘committed’ mining pipeline of 57 projects worth $41bn over the next three years that will require 20,767 employees to deliver. We must avoid a scenario where nationally significant mining projects are delayed by skills and labour shortages, competing for engineers, trades and skilled operators, with the $100bn worth of Commonwealth Public Infrastructure projects in Australia’s construction pipeline.

Australia’s resources and energy industry is facing new workforce demands at levels not seen. It is clear that securing the pipeline of skills to support mining and energy project growth to 2024 will be a significant challenge. Our labour market is in desperate need of skilled migration. We need to open up our borders and actively work to encourage skilled workers to come here.

Key stakeholders such as government, employers, unions and industry peak bodies need to collaboratively design a plan to secure a skilled workforce to deliver the 57 major resources and energy projects to eliminate the risk that will ensure Australian investment and the continued growth of our resources and energy sector. AREEA (Australian Resources and Energy Employer Association) Chief Executive Steve Knott said the industry would struggle to fulfil this new workforce demand without “creative solutions and a coordinated response.”

Lastly, you will have noted in the last four months the high rate of turnover within the ASX 300 of company Chairs (18) and NEDs (104) coming and going in the sector. This is due to a number of reasons that include COVID-19 fatigue, the desire for a fresh set of eyes and new blood as well as corporate activity. We also note the movement in and out in CEOs (38) within the sector and the recent diversity statistics within the sector 6% (4/70) compared to the broader ASX 300 7% (21/300); additionally, an increase of females to 18% of all Resources & Energy Sector employees, up from 17% in 2018-19.

Bradley Clyde

Partner